Mr. Vinay Paharia

Chief Investment Officer - Equity, PGIM Mutual Fund.

Vinay Paharia joined PGIM India AMC in January 2023 and is currently the Chief Investment Officer at PGIM India Mutual Fund. He has over 22 years of experience in equity market and fund management. He holds M.M.S, BCom and CFA (ICFAI) degrees. Vinay has been a growth investor and has followed a consistent investment philosophy of buying good quality and high growth companies at a reasonable price. This strategy has been an evergreen framework and has outperformed markets most of the times (but not all the time). His objective is to buy companies that are available at a price that may be slightly lower than the underlying fair value, which presents a greater potential upside over a five-year period. Vinay vouches for a disciplined, evidence-based investment approach over chasing short-term returns.

Please note we have published the answers as it is received from the Fund Manager of PGIM Mutual Fund.

Q1. With India’s valuation premium over other emerging markets moderating and GDP growth expected to remain strong (~6.8% in FY27), how do you assess the current risk-reward for long-term equity investors? Within this backdrop, which segments-large caps, mid caps, or small caps-appear relatively better positioned today from a valuation and earnings growth perspective?

Ans: Last few months have been a macro stress test - combining oil shock, capital outflows, currency pressures, AI related growth pangs and growth downgrades in a short span. However, we believe, many of these being transitory and would resolve itself with passage of time, timelines however are uncertain. More importantly, the above has resulted in a meaningful correction in the markets and much of the froth in valuations which was built has been taken away which is being reflected in the price. Largecaps and Smallcaps are now trading very close to their longer term averages in terms of valuation and risk-reward is much more balanced than before. However, Midcaps are still trading at moderately rich valuations and are hence less preferred compared to large caps and small caps. We believe, it is a good time to increase allocation to Indian equities. It is important to remember that timing is very difficult and investing when risk-reward is favorable is likely to be more fruitful. More importantly, the risk-reward is highly favorable for high growth and good quality business, wherein valuation as well as earnings growth both are in favor for long term investing.

Q2. With passive AUM continuing to rise in India, where do you believe active management can still consistently generate alpha? Are there specific market segments or conditions-such as higher dispersion or volatility-where active strategies have a clear edge over passive?

Ans: Active management's fundamental premise remains robust: markets are not completely efficient, and skilled managers can exploit these inefficiencies to generate risk-adjusted returns above benchmark indices. The strengths of active investing include:

1. Alpha Generation Potential: Skilled active managers can capitalize on market inefficiencies, behavioural biases, and information asymmetries that passive strategies cannot exploit. During periods of significant market stress or structural changes, active managers can potentially protect capital and identify opportunities thereby generating alpha.

2. Risk Management Flexibility: Active managers possess the ability to adjust portfolio risk dynamically, reducing exposure during periods of heightened volatility or when valuations appear stretched. This tactical flexibility can be particularly valuable during market transitions that indices cannot anticipate.

3. Access to Unique Opportunities: Active strategies can invest in securities or sectors before they enter major indices, potentially capturing returns during the inclusion process. They can also avoid or underweight deteriorating companies that indices must hold until they are removed.

We expect polarized performance from the markets. We expect high growth and high quality buckets to outperform while the low growth/quality bucket to underperform and give away the excesses which were built in FY24. Passive investing means there is some degree of exposure to low growth and low quality stocks as they make up a significant portion of Indexes. Active investing ensures conviction and exposure largely to high growth and high quality stocks.

Q3. As we approach the upcoming earnings season, what is your outlook on corporate earnings growth? Which sectors or themes are likely to drive the next phase of market performance, and where do you see the key downside risks?

Ans: We think we are once again likely to witness an earnings impact like that in the pandemic period. In March 2020 to June 2020 quarter (the first quarter of pandemic), we witnessed massive cuts in Nifty 50 Index 1-year forward earnings expectation, from a growth in double digits (in line with historical performance) to an almost 15% decline. However, once again, this is only likely to be transient (like the pandemic) and not structural. Hence we do not expect a material long term structural impact on the macroeconomic environment. The actual earnings compounded at 15% per annum from March 2020 to March 2026, highlighting the transient impact of the pandemic. We feel the longer term earnings trajectory is unlikely to be impacted even this time, with only a short term transient impact likely due to the current geo political environment. Even a massive cut in short-term earnings can only have a small impact on overall Fair Values of companies. This is because equities are growing annuities valued till perpetuity.

Overall fabric of the market constructive for growth + quality investing for the long term. Preferred sector plays are more domestic oriented – Consumption, Domestic financials, India Healthcare, Telecom. Cautious/Negative on I.T, deep cyclicals, Energy and Utilities

Q4. SIP inflows have remained resilient, touching record highs even during volatile phases. Do you see this as a structural shift in investor behaviour? During market corrections, would you advise investors to maintain, increase, or rebalance SIP allocations-and what factors should guide that decision?

Ans: Investment decisions are shaped not only by returns or market data, but also by individual behaviour. Risk tolerance, time horizon, and emotional responses play a significant role in how investors act, especially during volatile markets. We advise investors to maintain staggered investments for all segments of the market.

Periods of geopolitical uncertainty, such as the conflict unfolding today, often lead to higher market volatility and heightened investor reactions. It is common for investors to consider redeeming investments prematurely, trying to time the market, or pausing allocation decisions altogether. While these responses are natural, history shows that emotionally driven decisions

often work against long-term financial goals. Our internal study of Nifty 500 TRI shows that investors who stayed invested 04-Sep-2001 to 31-Dec-2025) during this period, earned 17.33% return while investors who missed the best 20 days ended up earning just 11.06%. This means that investor who stayed invested, (assuming a lumpsum investment of 1 lakh), made Rs 48.77 lakh at the end of 24.32 years. The investor who missed 20 days accumulated Rs 12.82 lakh, a difference of (Rs-35.95 lakh).

Q5. Many investors chase recent outperformers, especially in mid- and small-cap funds, often misaligning with their true risk appetite. What framework would you recommend for selecting equity funds and ensuring portfolios remain aligned with risk tolerance? How can investors stay disciplined through market cycles?

Ans: We have been strong proponents of Growth Investing in India. Our definition of Growth Investing is as follows:

"Investing in a well-diversified portfolio of companies that demonstrate above average growth in business, while generating above average return on equity, purchased at a reasonable price"

Growth investing is all about buying good businesses at fair price. Returns for growth investors are largely driven by earnings growth. Growth investors do not bet on valuation re-rating, but on fair value growth. India is one of the fastest growing large economies in the world. Thus, we have a higher probability of finding superior growth companies in India. We have a large number of companies generating higher than their cost of equity, thereby creating superior shareholder value. We have also witnessed IPOs of a large number of good quality and high growth new age businesses in Indian bourses. Indian companies on average have generated a healthy return on equity (RoE) while growing at a reasonable pace. Over the Long term (two decade) average RoE generated by Top 500 companies in India is 15%. Similarly, long term average sales growth has been 12% for the same set.

We tend to be overweight on the Consumer Discretionary and Healthcare Sectors, as the stocks within these sectors align with our investment philosophy.

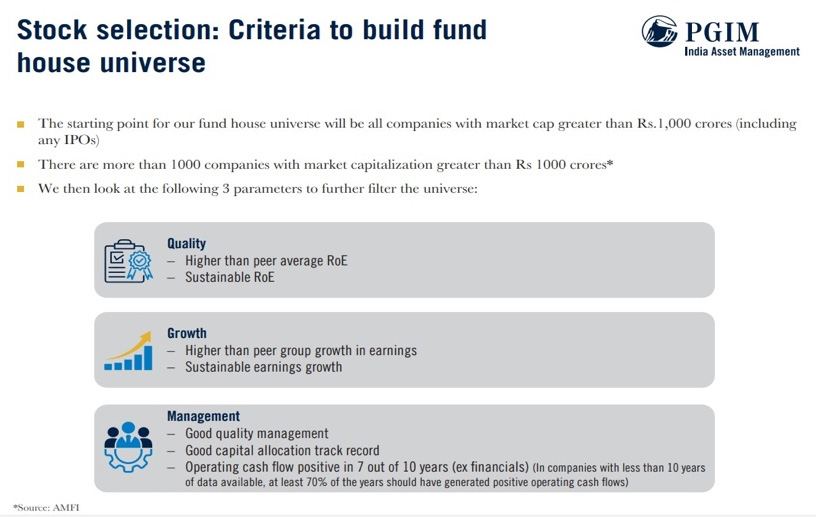

Q6. What are the non-negotiable factors your team looks for when selecting stocks? Specifically, how do you evaluate management quality and governance to ensure businesses can sustain performance across cycles?

Ans: Our framework excludes low-growth and low-quality stocks, and it is applicable on all sectors.

Our evaluation of management quality is in conjunction with the quantitative measures stated above and promoter background checks, as well as internal risk triggers. We also take a holistic view from the Fixed Income Team on rating wherever applicable and relevant

Source: Internal Research

Mutual fund investments are subject to market risks, read all scheme-related documents carefully.